A new report by noted maritime economist John Martin, PhD., and Martin Associates, commissioned by the Pacific Maritime Association, highlights how record container volumes at the Ports of Los Angeles and Long Beach (the San Pedro Bay ports) and other factors are diminishing the advantages these gateways have traditionally had over competitors on the Atlantic and Gulf Coasts. Building on Martin Associates’ recent supply chain research, the latest report shows how this trend could gain momentum, negatively impacting the myriad workers, businesses and consumers who rely on West Coast ports.

Congestion due to record-high container volumes in Southern California, coupled with the growing capacity at East and Gulf Coast ports, are shifting the market share of Asian imports away from the West Coast. This has created a striking impact on trans-Pacific trade: By the end of 2021, container transit time from China to the Port of New York and New Jersey was 12 days faster than to the San Pedro Bay ports — a stark reversal of the hallmark speed that Southern California has long offered due to its relative proximity to Asia.

Atlantic and Gulf Coast ports are expected to handle an increasing share of this cargo unless San Pedro Bay container terminals increase throughput capacity to handle further container volume growth. In the near term, however, these rival ports have little spare capacity, so any work disruptions by West Coast longshore workers during coming contract negotiations would re-aggravate supply-chain delays. Recently, congestion has been growing at some East Coast ports. As of April 7, there were 18 ships waiting to berth at the Port of Charleston and 12 ships outside the Port of Norfolk, carrying a combined total of 209,000 TEUs, according to Port Technology International.

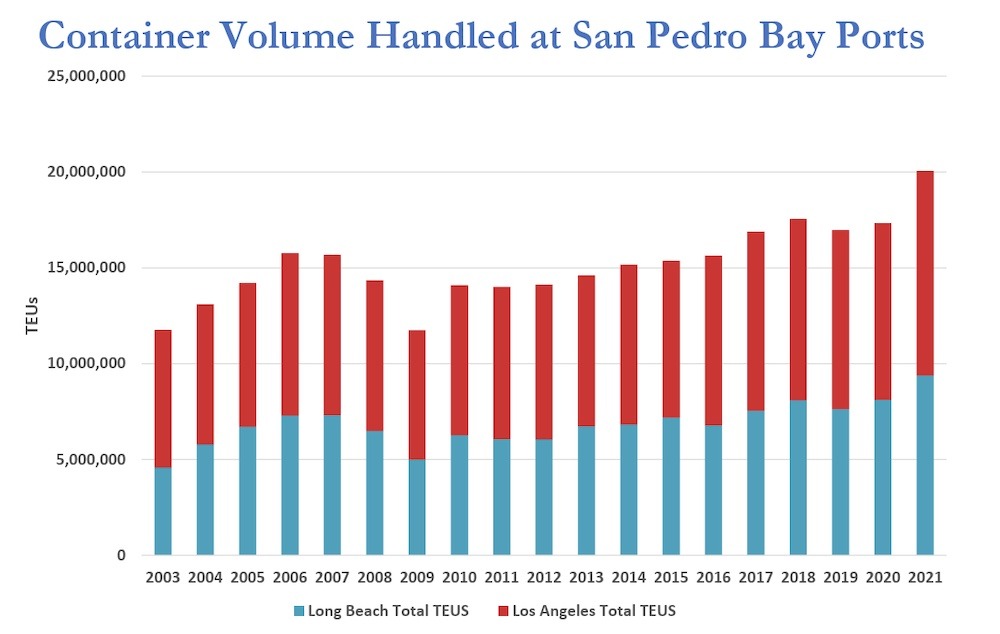

Historic Supply Chain Congestion: In 2021, containers volume at the San Pedro Bay ports reached a record 20 million TEUs, up from the 17.2 million TEUs the ports handled on average between 2017 through 2020. This surge has created a system-wide supply chain collapse, with constraints at all levels, including marine terminals; container yards; warehouses and distribution centers; chassis and truck driver availability; and intermodal capacity, all worsened by pandemic-related labor shortages.

This congestion has increased the average dwell time of containers (the length of time a container remains on the terminal after it is discharged) to 8.4 days in November 2021, compared to the historical average of 3.3 days. Driven in part by the rise in e-commerce – which requires more distribution center space than cargo bound for brick-and-mortar stores – warehouse shortages have been an increasingly key bottleneck in Southern California, falling to a vacancy rate of less than 1% in Q4 of 2021.

Growth of Major Atlantic and Gulf Coast Ports: The large number of container vessels at anchor outside the San Pedro Bay ports is driving importers to divert cargo from Asia to Atlantic and Gulf Coast ports. Martin Associates attributes this shift to a range of factors, including the fluidity of East Coast ports relative to Southern California; faster service between Asia and New York than congested San Pedro Bay ports; and anticipation of renewed labor disruptions on the West Coast.

Labor concerns have market-share gains by Atlantic and Gulf Coast ports since 2002, when a West Coast port shutdown during contract negotiations prompted a structural supply chain shift away from the Pacific gateways. Notably, during most of the pandemic, market share at the Pacific Southwest (PSW) ports of Los Angeles and Long Beach remained stable, as shown below. But in the last quarter of 2021, when terminal congestion and warehouse scarcity peaked in Southern California, market share fell rapidly in favor of North Atlantic Coast ports. Capacity at East and Gulf Coast ports is now strained, likely impacting the national supply chain. Yet over the long term, terminal capacity enhancements as well as increased rail and warehouse capacity are expected to establish these ports as attractive alternatives to the West Coast.

Addressing the Challenges Ahead: The system-wide supply chain disruptions since 2020 have enormous implications for the Los Angeles and Long Beach ports. These gateways have lost market share as Atlantic and Gulf Coast ports increasingly provide time and cost advantages for Asian cargo destined for Midwestern states. The San Pedro Bay ports are operating near capacity, and Martin Associates found that unless they can expand capacity through densification and other efficiencies to handle future growth, their market-share losses could accelerate. Further, it is critical that upcoming contract negotiations between PMA and the International Longshore and Warehouse Union do not result in work disruptions.